Clustering stocks can substantially enhance your trading strategies and assist in managing diversification with professionalism. The concept of clustering involves the grouping of stocks according to their fundamental characteristics and/or their price movements.

A common way to classify stocks is by sector. If you haven’t already, consider making sector diversification a key part of your investment strategy. This involves holding stocks across different sectors to prevent over-reliance on one sector’s performance. While all these methods are used for risk management, clustering stocks by selecting our own features definitely adds another dimension to our trading style.

How to trade based on clusters

Pairs Trading and Statistical Arbitrage

This strategy is based on finding stocks that typically move in tandem but have temporarily diverged. When one stock (stock A) surges while the other (stock B) lags, you take a short position in stock A and a long position in stock B. Statistically, these stocks tend to converge again over time, allowing you to capture profits as their prices realign. While this approach is most commonly used with pairs of stocks, it can also be extended to a group by going long on those that have under-performed and short on those that have outperformed.

Market Regime Detection

Grouping can help you identify real-time market trends—whether bullish, bearish, or sideways—by clustering periods that share similar characteristics in price movement, volatility, or trading volume. Once a trend is recognised, you can adjust your trading strategy accordingly:

- In a bullish cluster, go for long positions or momentum strategies.

- In a bearish cluster, use shorting or protective hedges.

- In a sideways cluster, go for mean-reversion or range-bound strategies.

Identify opportunities

Cluster analysis can complement or even replace your existing stock screeners. If you already use specific criteria to filter stocks for potential opportunities, it’s a good idea to also examine which stocks are grouped together with the one you’re analysing. This approach might uncover promising stocks that you haven’t considered yet or that your screener may have missed.

But how can we do that?

Gather the data

We will use the EODHD APIs for pricing and fundamentals, but before that let’s do the imports and get all the SP500 stocks:

import requests

import pandas as pd

import requests_cache

import os

from matplotlib import pyplot as plt

from tqdm import tqdm

import warnings

api_token = os.environ.get('EODHD_API_TOKEN')

def get_sp500_tickers():

INDEX_NAME = 'GSPC.INDX'

url = f'https://eodhd.com/api/mp/unicornbay/spglobal/comp/{INDEX_NAME}'

query = {'api_token': api_token, "fmt": "json"}

data = requests.get(url, params=query)

if data.status_code != 200:

tqdm.write(f"Error: {data.status_code}")

tqdm.write(data.text)

return []

data = data.json()

df_stocks = pd.DataFrame(data['Components']).T.reset_index()

df_stocks.to_csv('csv/stocks_universe.csv', index=False)

tickers = df_stocks['Code'].tolist()

return tickers

# Get S&P 500 tickers

sp500_tickers = get_sp500_tickers()Now lets get the prices of all the SP500 stocks from 2024 and store them in a dataframe named sp_500_prices_df

start_date = '2024-01-01'

sp_500_prices_df = pd.DataFrame()

for ticker in tqdm(sp500_tickers, desc="Fetching ticker data"):

try:

# Construct the API URL

ticker_code = f"{ticker}.US"

url = f'https://eodhd.com/api/eod/{ticker_code}'

# Set query parameters

query = {

'api_token': api_token,

'fmt': 'json',

'from': start_date

}

response = requests.get(url, params=query)

if response.status_code == 200:

# Parse the JSON response

data = response.json()

# Convert to DataFrame

ticker_df = pd.DataFrame(data)

# Extract date and adjusted_close

if 'adjusted_close' in ticker_df.columns:

prices = ticker_df[['date', 'adjusted_close']].copy()

prices.set_index('date', inplace=True)

# Rename the column to the ticker symbol

prices.rename(columns={'adjusted_close': ticker}, inplace=True)

# Join with the main DataFrame

if sp_500_prices_df.empty:

sp_500_prices_df = prices

else:

sp_500_prices_df = sp_500_prices_df.join(prices, how='outer')

else:

tqdm.write(f"No adjusted close data available for {ticker}")

else:

tqdm.write(f"Error fetching data for {ticker}: {response.status_code}")

tqdm.write(response.text)

except Exception as e:

tqdm.write(f"Exception occurred while processing {ticker}: {str(e)}")

returns = sp_500_prices_df.pct_change().dropna()The next step is to get into the fundamentals. We’ll enrich our S&P 500 stocks dataframe by adding columns for Sector, Industry, Market Capitalisation, and P/E ratio—details that will be essential for our grouping later on. For Market Capitalisation, you’ll see that I categorize it into more intuitive groups, such as Mega, Large, and so on, to make the data easier to interpret.

df = pd.DataFrame()

# Fetch fundamental data for each ticker

for ticker in tqdm(sp500_tickers, desc="Fetching fundamental data"):

try:

# Construct the API URL

ticker_code = f"{ticker}.US"

url = f'https://eodhd.com/api/fundamentals/{ticker_code}'

# Set query parameters

query = {

'api_token': api_token,

'fmt': 'json'

}

# Make the API request

response = requests.get(url, params=query)

# Check if the request was successful

if response.status_code == 200:

# Parse the JSON response

data = response.json()

# Extract the required metrics

metrics = {

'Ticker': ticker,

'Name': data.get('General', {}).get('Name', None),

'Sector': data.get('General', {}).get('Sector', None),

'Industry': data.get('General', {}).get('Industry', None),

'Market Capitalisation': data.get('Highlights', {}).get('MarketCapitalization', None),

'P/E Ratio': data.get('Highlights', {}).get('PERatio', None)

}

# Add to the dataframe

df = pd.concat([df, pd.DataFrame([metrics])], ignore_index=True)

else:

tqdm.write(f"Error fetching fundamental data for {ticker}: {response.status_code}")

tqdm.write(response.text)

except Exception as e:

tqdm.write(f"Exception occurred while processing fundamental data for {ticker}: {str(e)}")

# Define capitalization bins and labels

bins = [0, 1e10, 1e11, 1e12, 1e13]

labels = ['Small (<10B)', 'Medium (10B-100B)', 'Large (100B-1T)', 'Mega (>1T)']

# Create a new column for capitalization bins

df['Cap_Bin'] = pd.cut(df['Market Capitalisation'], bins=bins, labels=labels)We will also add in the same dataframe the 6-month volatility, which will later be used as a feature for grouping.

sp_500_prices_df.index = pd.to_datetime(sp_500_prices_df.index)

# Sort by date

sp_500_prices_df = sp_500_prices_df.sort_index()

# Get the last 6 months of data

six_months_ago = sp_500_prices_df.index[-1] - pd.DateOffset(months=6)

six_month_prices = sp_500_prices_df[sp_500_prices_df.index >= six_months_ago]

# Calculate daily returns

daily_returns = six_month_prices.pct_change().dropna()

# Calculate volatility (standard deviation of returns)

volatility = daily_returns.std() * (252 ** 0.5) # Annualized volatility

# Add volatility to the fundamentals dataframe

for ticker in sp500_tickers:

if ticker in volatility.index:

mask = df['Ticker'] == ticker

df.loc[mask, '6-Month Volatility'] = volatility[ticker]Clustering with fundamentals

With all the required data in place, we’ll now organise the stocks into 11 clusters. I selected this number because there are 11 sectors in the S&P 500, and I’m interested to see how closely our clusters will match the actual sector classifications.

In a nutshell:

- We define the features and normalise them

- In case there are missing data we impute them

- We use Principal Component Analysis (PCA) to reduce the complexity

- We use K-Means and group them into 11 clusters

# Preprocessing

features = df[['Market Capitalisation','P/E Ratio','6-Month Volatility']]

# Normalize features

from sklearn.preprocessing import StandardScaler

scaler = StandardScaler()

scaled_data = scaler.fit_transform(features)

# Impute Missing Data

# The most common approach is to fill missing values with the mean, median, or another strategy using SimpleImputer from scikit-learn:

from sklearn.impute import SimpleImputer

imputer = SimpleImputer(strategy='mean') # or 'median'

imputed_data = imputer.fit_transform(features)

from sklearn.preprocessing import StandardScaler

from sklearn.decomposition import PCA

scaler = StandardScaler()

scaled_data = scaler.fit_transform(imputed_data)

pca = PCA(n_components=0.95)

principal_components = pca.fit_transform(scaled_data)

from sklearn.cluster import KMeans

k = 11 # Typical for sector-based clustering

model = KMeans(n_clusters=k)

clusters = model.fit_predict(principal_components)

df['ClusterFeatures'] = clustersLet’s plot and see how the stocks are distributed per sector:

# Group by Sector and ClusterCorrelation, then count

sector_cluster_counts = df.groupby(['Sector', 'ClusterFeatures']).size().reset_index(name='Count')

# Pivot for a matrix view

pivot_table = sector_cluster_counts.pivot(index='Sector', columns='ClusterFeatures', values='Count').fillna(0).astype(int)

# Create a stacked bar chart

plt.figure(figsize=(14, 10))

pivot_table_percentage = pivot_table.div(pivot_table.sum(axis=1), axis=0) * 100

# Plot stacked bar chart

pivot_table_percentage.T.plot(kind='bar', stacked=True, figsize=(14, 10), colormap='tab20')

plt.title('Percentage Distribution of Sectors across Correlation Features', fontsize=16)

plt.xlabel('Correlation Features', fontsize=14)

plt.ylabel('Percentage', fontsize=14)

plt.legend(title='Sector', bbox_to_anchor=(1.05, 1), loc='upper left')

plt.tight_layout()

plt.show()

Not so insightful. The groups are unbalanced and not related to sector. So lets use some box plots:

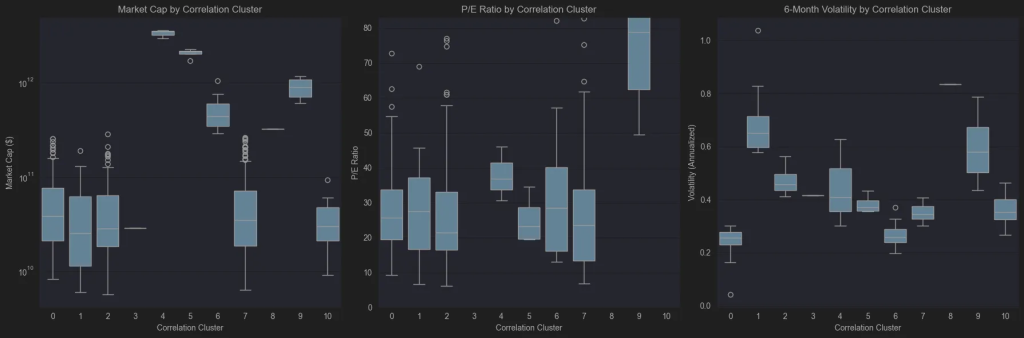

import matplotlib.pyplot as plt

import seaborn as sns

# Set up the figure with 3 subplots side by side

fig, axes = plt.subplots(1, 3, figsize=(18, 6))

# Boxplot for Market Capitalization

sns.boxplot(x='ClusterFeatures', y='Market Capitalisation', data=df, ax=axes[0])

axes[0].set_title('Market Cap by Correlation Cluster')

axes[0].set_ylabel('Market Cap ($)')

axes[0].set_xlabel('Correlation Cluster')

# Use log scale for Market Cap due to wide range

axes[0].set_yscale('log')

# Boxplot for P/E Ratio

sns.boxplot(x='ClusterFeatures', y='P/E Ratio', data=df, ax=axes[1])

axes[1].set_title('P/E Ratio by Correlation Cluster')

axes[1].set_ylabel('P/E Ratio')

axes[1].set_xlabel('Correlation Cluster')

# Set a reasonable y-limit to handle outliers

axes[1].set_ylim(0, df['P/E Ratio'].quantile(0.95))

# Boxplot for 6-Month Volatility

sns.boxplot(x='ClusterFeatures', y='6-Month Volatility', data=df, ax=axes[2])

axes[2].set_title('6-Month Volatility by Correlation Cluster')

axes[2].set_ylabel('Volatility (Annualized)')

axes[2].set_xlabel('Correlation Cluster')

plt.tight_layout()

plt.show()

What I can see from the box plots in a first glance is:

- Group 4 consists of Apple, Nvidia, and Microsoft—clearly representing the largest stocks by market capitalization. Group 5 features the next tier of giants, including Google, Amazon, and Meta, while Group 9 brings together Broadcom, Lilly, Oracle, and Tesla. The accompanying boxplot of P/E Ratios shows that the algorithm effectively distinguished these mega-cap companies based on their P/E Ratio.

- It’s also noteworthy that groups 0, 1, 2, 7, and 10 are predominantly made up of small- and mid-cap stocks. Group 10 stands out with the highest P/E ratio and shows moderate to low volatility, while the remaining four groups are mainly distinguished by their varying levels of volatility.

I use this method when I see a stock I like and want similar stocks with comparable features. I don’t want to miss an opportunity if I’m right, as other stocks in the same group could be even better options. This may seem like it could be done easily with a good screener. But with more features and groups, this method can quickly generate groups of stocks sharing the same features, expanding your search and providing better insights for decision-making.

Clustering with price correlation

Now we move to something more interesting and familiar – the price action! We’ll perform and other clustering process using each stock’s correlation, grouping (again into 11 clusters) stocks based on their price movements.

In a nutshell:

- Calculate the correlation matrix.

- Convert the correlations into distances.

- Perform hierarchical clustering using the average linkage method.

import numpy as np

corr_matrix = returns.corr()

distance_matrix = np.sqrt(2 * (1 - corr_matrix))

distance_matrix

from scipy.cluster.hierarchy import linkage, dendrogram

# Average linkage often performs best for financial data[1][5]

Z = linkage(distance_matrix, method='average')

from scipy.cluster.hierarchy import fcluster

# t is the number of clusters

clusters = fcluster(Z, t=11, criterion='maxclust')

df.to_csv('csv/sp500_clustered.csv', index=False)

df['ClusterCorrelation'] = clustersNow let’s plot the same bar chart based on the sectors.

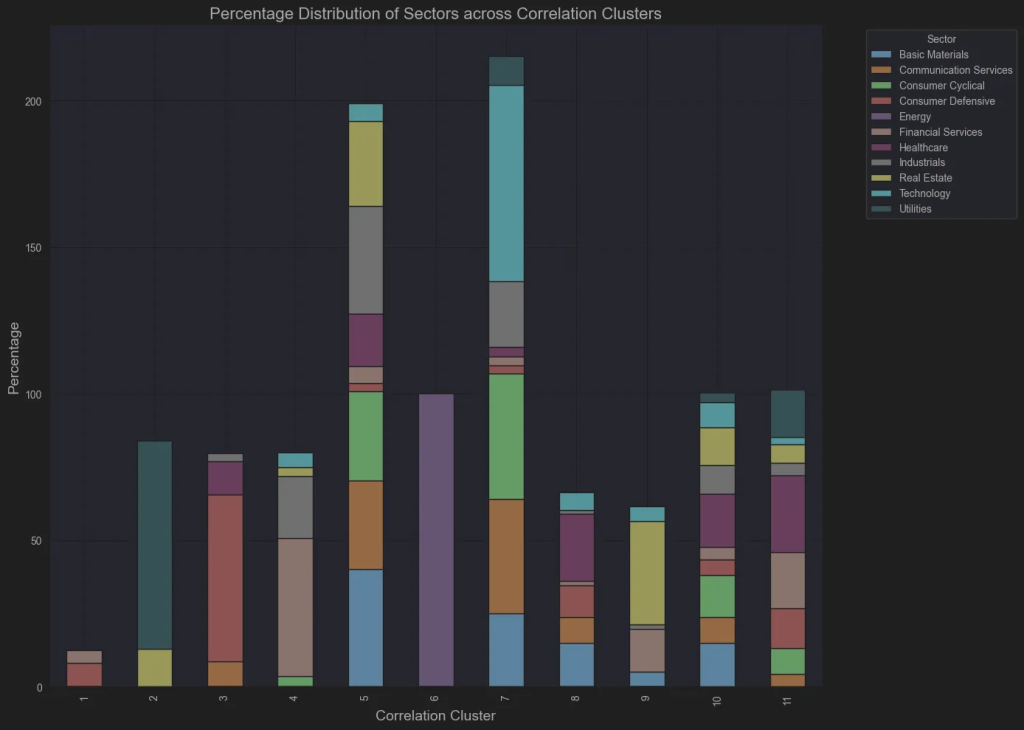

# Group by Sector and ClusterCorrelation, then count

sector_cluster_counts = df.groupby(['Sector', 'ClusterCorrelation']).size().reset_index(name='Count')

# Pivot for a matrix view

pivot_table = sector_cluster_counts.pivot(index='Sector', columns='ClusterCorrelation', values='Count').fillna(0).astype(int)

# Create a stacked bar chart

plt.figure(figsize=(14, 10))

pivot_table_percentage = pivot_table.div(pivot_table.sum(axis=1), axis=0) * 100

# Plot stacked bar chart

pivot_table_percentage.T.plot(kind='bar', stacked=True, figsize=(14, 10), colormap='tab20')

plt.title('Percentage Distribution of Sectors across Correlation Clusters', fontsize=16)

plt.xlabel('Correlation Cluster', fontsize=14)

plt.ylabel('Percentage', fontsize=14)

plt.legend(title='Sector', bbox_to_anchor=(1.05, 1), loc='upper left')

plt.tight_layout()

plt.show()

Let’s discuss this bar chart:

- Energy stocks are one cluster, indicating that this is a highly distinctive sector that moves together!

- Most Utility stocks in group 2 are from the Regular Electric industry, highlighting its distinct behavior within the sector.

- All the Mega stocks are in Group 7, except Berkshire, which is in Group 9. Nearly all technology stocks are also in Group 7, underscoring tech’s dominant role in the market.demonstrating that technology is the primary driver of the market.

What to do next

In the scope of this post, it is not so easy to examine all the possibilities of the clustering method. However, with some minor changes (or a bit more) of the above code, you can experiment and find insightful information that will guide you towards your personal trading edge:

- Add more features: dividend yield, debt/equity, revenue growth.

- Use technical indicators: RSI, MACD, moving averages.

- Incorporate alternative data: news sentiment, ESG scores.

- Apply clustering to rolling time windows.

- Build cluster-based stock screeners.

- Set up alerts for cluster composition changes.

- Automate clustering pipeline with scheduled updates.

Thanks for reading!